The pricing resilience of European safe assets

The pricing resilience of European safe assets

0:00 minThe issuance of European safe assets boomed when governments launched hefty support programmes during the Covid-19 pandemic. Although market fluctuations opened a pricing gap between AAA-rated European safe assets and sovereigns in 2022, this has narrowed recently. In this blog, we take a look at this trajectory to explain its drivers. We continue to see the benefits of joint European debt given calls to support growth and resilience through joint European borrowing.

European governments adopted economic support packages totalling €1.29 trillion when the Covid-19 pandemic struck in early 2020, triggering a quantum leap in the issuance of European bonds. The first package, worth an estimated €540 billion, involved the European Stability Mechanism (ESM), the European Investment Bank, and the European Commission. The second, Next Generation EU, has a combined firepower of €750 billion in grants and loans. [1]

This move towards a more central-like structure of debt management created a sizeable amount of European safe assets. Markets need safe assets for the proper functioning as a store of value, guarantee, and pricing benchmark. Debt financed by highly rated European institutions lowers interest costs for many countries and promotes region-wide convergence and economic stability. The combined stock of European safe assets surged from billions to trillions, passing the €1 trillion mark in March 2024.[2]

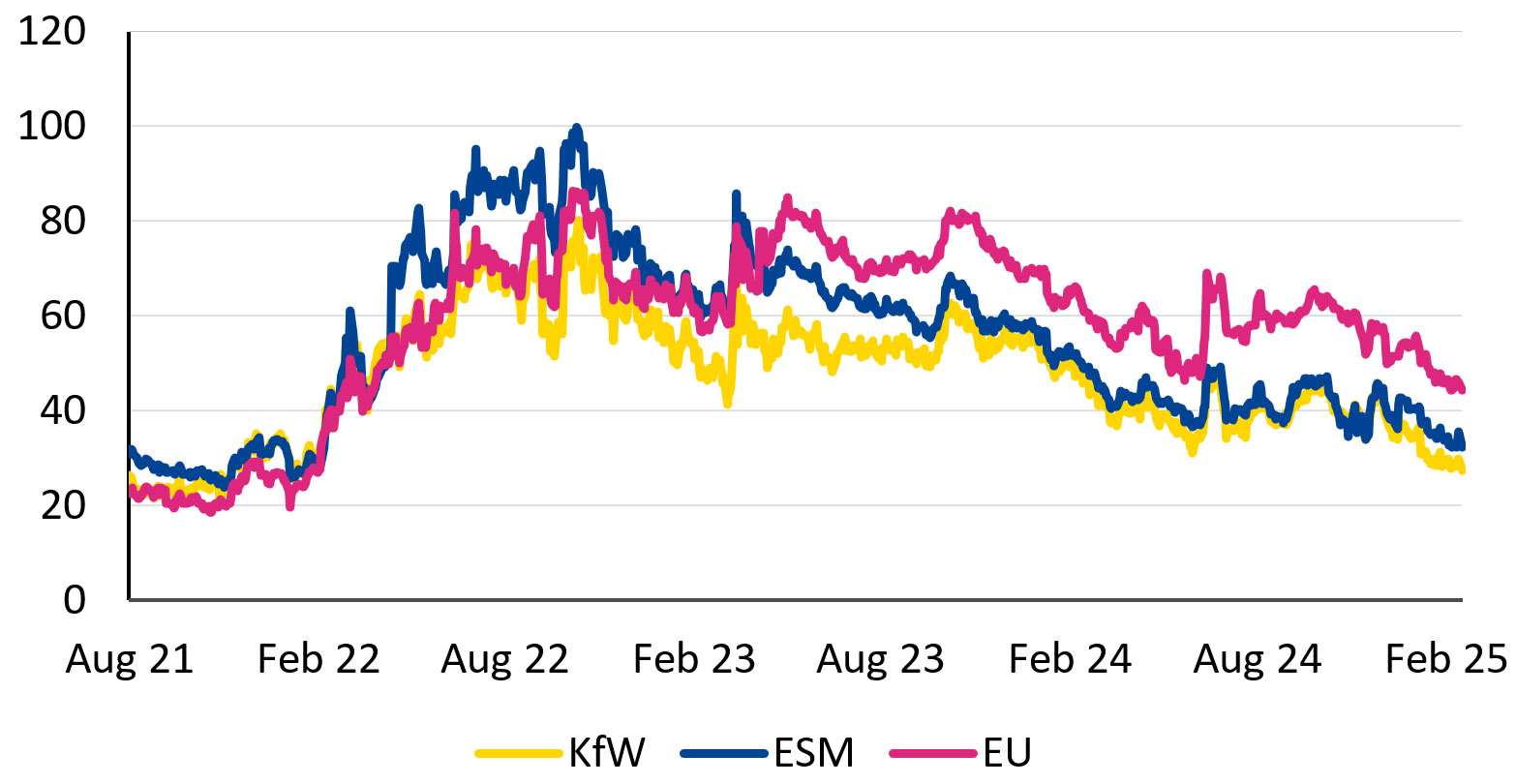

Borrowing costs of European supranational issuers have fluctuated in recent years, prompting a debate as to the possible drivers (Figure 1).

Figure 1: European supranational bond yields increased relative to Bunds in 2022 but then reversed

10-year bond spreads versus Germany

(in basis points)

Note: KfW is a German state-owned investment and development bank, an issuer of bonds guaranteed by the German state.

Source: Bloomberg

An in-depth look at the spread history

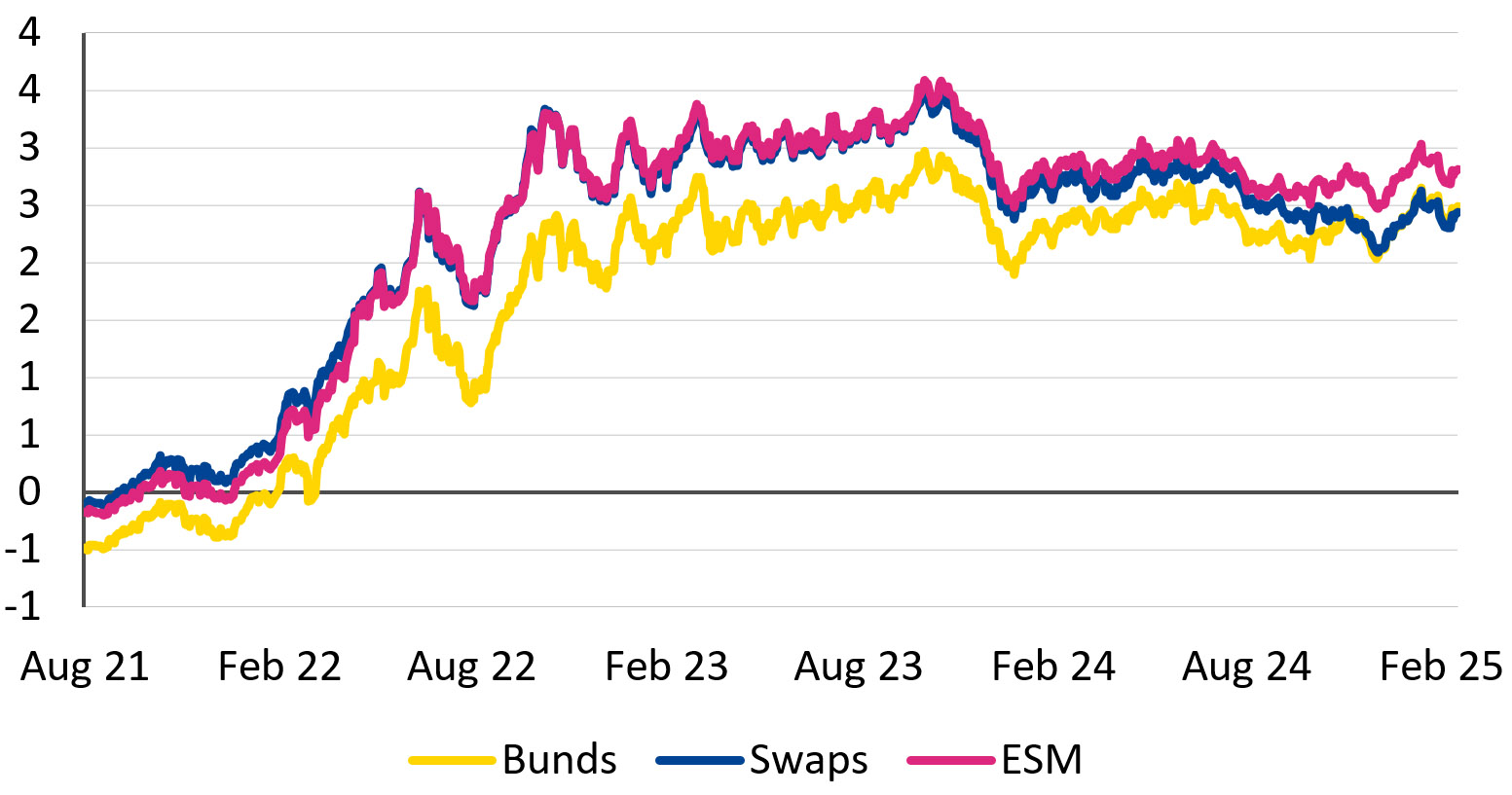

Some pundits claimed that wider European supranational spreads were driven by doubts about their creditworthiness and the uncertainty of the EU as a new large issuer. We find, instead, that the widening and subsequent reversal was mainly a consequence of changes in the spread between German government bond (Bund) yields and swap rates.[3] European supranational yields more closely followed swap rates, as markets price supranational bonds based on these rates, while Bund yields increased less and remained relatively lower through 2022 and 2023 (Figure 2).

Figure 2: European supranational bond yields more closely followed swap rates

10-year bond yields and swap rates

(%)

Source: Bloomberg

In 2022, a gap between Bunds and swap rates widened, in part because of the scarcity of free-floating[4] Bunds on the markets. The share of central bank holdings of Bunds peaked in 2022, with nearly half locked up on the Eurosystem’s[5] balance sheet. The scarcity of available bonds may have pushed bond prices higher and yields lower relative to swap rates. In the meantime, the European Central Bank (ECB) started raising interest rates, pushing swaps higher, also contributing to a divergence between swap rates (higher) and bond yields (lower). The ECB may have also held a large share of supranational bonds, but those yields still remained aligned with swap rates.

By 2024, this trend went into reverse. Monetary policy has been easing, bringing swap rates down, while bond supply has been rising and putting upward pressure on yields. Bond yields have risen across the board since October, with German and French government yields rising by about 40 basis points as of February. Consequently, the difference between swap rates and Bund yields has evaporated (Figure 3). [6] European supranationals showed resilience with a more limited increase in yields of around 30 basis points, broadly in line with the rise in KfW’s yields which carries a credit risk seen as directly aligned with the German sovereign.

Figure 3: The difference between swap rates and Bund yields has closed in 2024

Difference between 10-year swap rates and Bund yields

(in basis points)

Source: Bloomberg

The narrowing of swap spreads is not unique to the euro area, and longer-term structural factors may have played a role. Swap spreads used to be a measure of risks in the banking sector, as swaps are traded by banks and reflected counterparty risk, but this is no longer the case. Given new regulations since the global financial crisis on derivatives’ counterparty risk management, this feature is now less salient and offers less justification for swap rates above AAA bond yields.

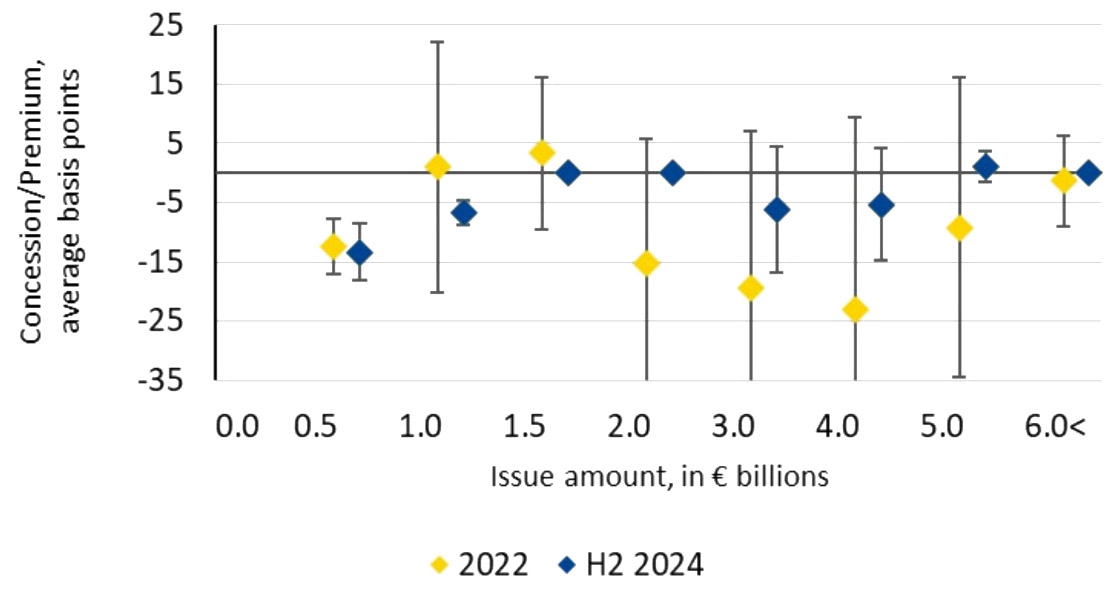

Recently, bond yields seem to have become more sensitive to supply dynamics. The concessions at large bond auctions increased in 2024 compared to 2022, showing that issuers have to pay a higher premium to place their bonds (Figure 4).

Figure 4: Investors have become more sensitive to the size of issuance in 2024 compared to 2022

German government bond auctions, 5-15 year maturity

Note: The chart shows concessions/new issue premium at auctions of German government bonds with maturities between 5 and 15 years.

Source: ESM calculations based on Bloomberg and Refinitiv data

The scarcity seen in 2022 appeared more specific to German government bonds, but the increase in net supply in 2024 was more broad-based. While a slight decrease in government budget deficits is expected, the Eurosystem’s balance sheet reduction adds to the volume of bonds that financial markets must absorb. As the ECB stops reinvesting the proceeds from its maturing bonds, governments need to raise more financing from private investors. Overall, the net supply of government bonds to be absorbed by financial markets is set to increase in the coming years, and investors may demand higher yields as a result. We see this as less of a concern for European supranational issuers, but a cautionary sign for member states with large financing needs.[7]

A powerful tool for debt management

Because European safe assets enjoy the market’s confidence, they have helped provide affordable funding for the benefit of joint European initiatives. Their status is backed by significant joint commitments from all participating EU and euro area member states – based on capital, contributions, and guarantees. Safe assets like ESM bonds can ensure lower borrowing costs than the weighted average of euro area sovereigns. [8] The increase in outstanding bonds of European issuers is a valuable addition to the management of the European economy, not only by making funds more available, but also by providing such safe assets to anchor the markets.

Nevertheless, further steps are needed to turn European safe assets into a market benchmark for sovereign issuers. Most importantly, there would need to be sizeable permanent issuance activity – something currently not a given. European Commission issuance is largely linked to Next Generation EU, which is temporary, while the size of bond issuance by the European Financial Stability Facility and ESM is tapering. Over time, the pool of available European safe assets will shrink. Any move to build it back up would require a political decision by EU Member States.

Acknowledgements

The authors would like to thank Ivan Smerdjiev, Elisabetta Vangelista, Ioannis Vazouras and Stephane Vincent for contributions to this blog post, and Raquel Calero for the editorial review.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager