Predicting trouble: a new analytical tool to monitor bank asset quality

Non-performing loans (NPLs) are a key metric to assess the health of the banking sector. When NPL levels are low, banks can manage their capital more effectively supporting their ability and willingness to lend to the real economy. A manageable stock of NPLs makes banks less vulnerable to external shocks and more attractive to new investors, contributing to preserve financial stability.

Following two crises, euro area banks have gone through an impressive balance sheet strengthening that brought NPLs to historically low levels. Thanks to this hard-won resilience, the euro area banking sector appears now well positioned to navigate the challenges posed by a rapidly evolving risk landscape. However, some recent signs of asset quality deterioration raise the question about potential challenges ahead.

A novel framework developed at the ESM can help us answering this question by providing a forward-looking measure of risks to asset quality. The tool points to a system-wide resilience of the euro area banks in the current macro financial environment, notwithstanding some potential NPL increases in a few banks exposed to fragile sectors.

From peaks to troughs: significant NPL reductions, but new risks emerging

Non-performing loans have several negative effects on banks’ balance sheet. Banks consider a loan as “non-performing” when a borrower fails to honour the scheduled payments of principal or interest for a specified period. In the euro area, NPLs peaked in 2014 (8% of all loans) when severe economic downturns brought on by the global financial crisis and the European sovereign debt crisis spiked unemployment rates and stifled borrowers’ repayment capacity. This compounded with banks’ poor credit assessment and aggressive lending practises in the years before the crises, ultimately causing a sharp rise in NPLs in most euro area countries. Asset quality deterioration varied significantly among banks.

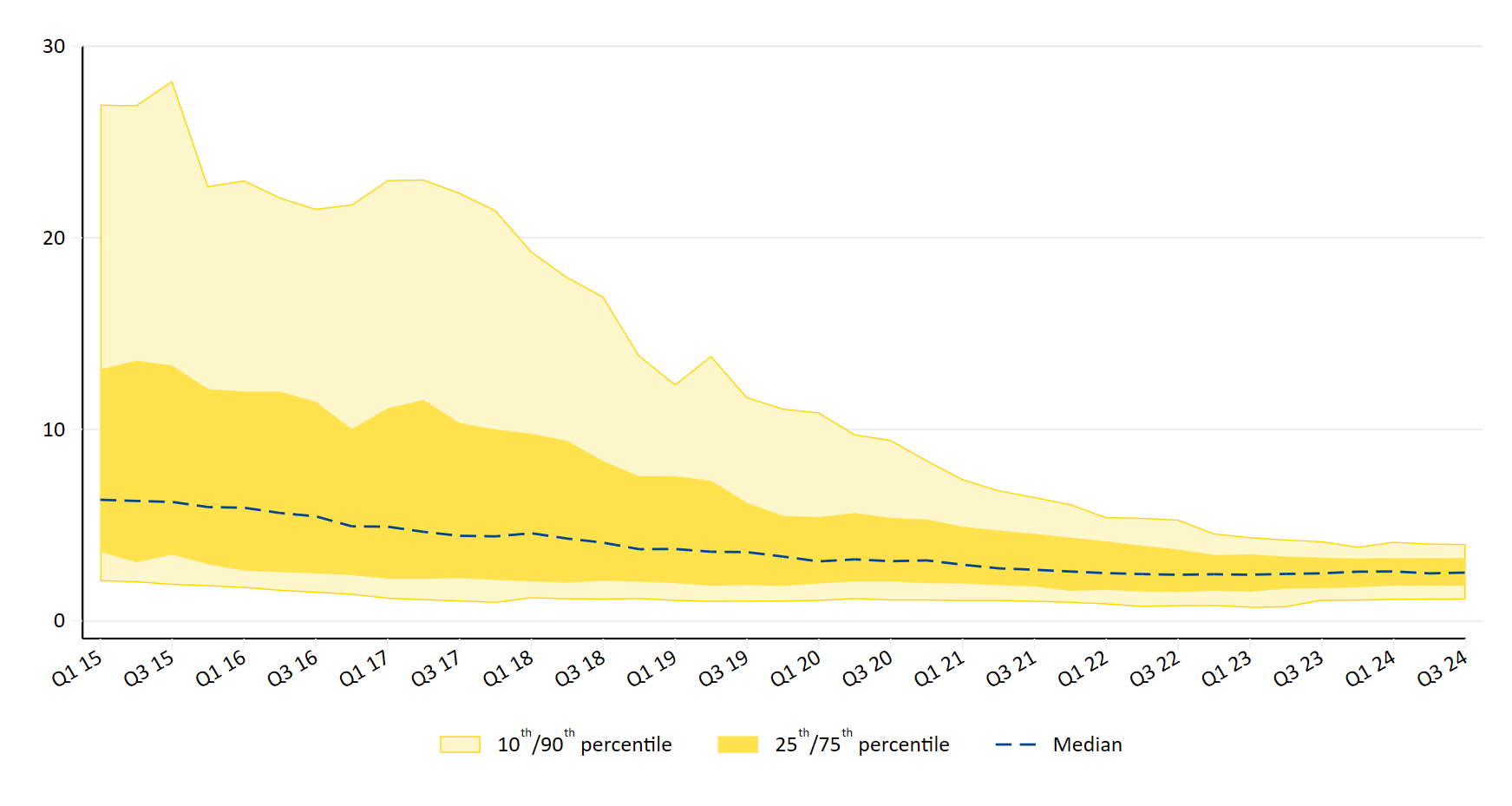

Thanks to regulatory interventions and significant banks’ efforts to clean up their balance sheets, NPLs have declined to historical lows at approximately 2.3% of total loans in the third quarter of 2024. Since 2015, banks with high NPL ratios have seen their bad quality loan books continuously shrinking over time (Figure 1). Still, banks with good quality loan books have recently begun to show signs of asset quality deterioration.

Figure 1: NPL ratio dispersion has significantly narrowed since 2015

(NPL ratios, in %)

Notes: The shaded area represents the range of NPL ratios in our sample of banks. The consistent decline in the 90th percentile shows improved NPL ratios, but recent uptick since 2023 in the 10th percentile warns of asset quality deterioration.

Source: ESM calculations based on Fitch Connect

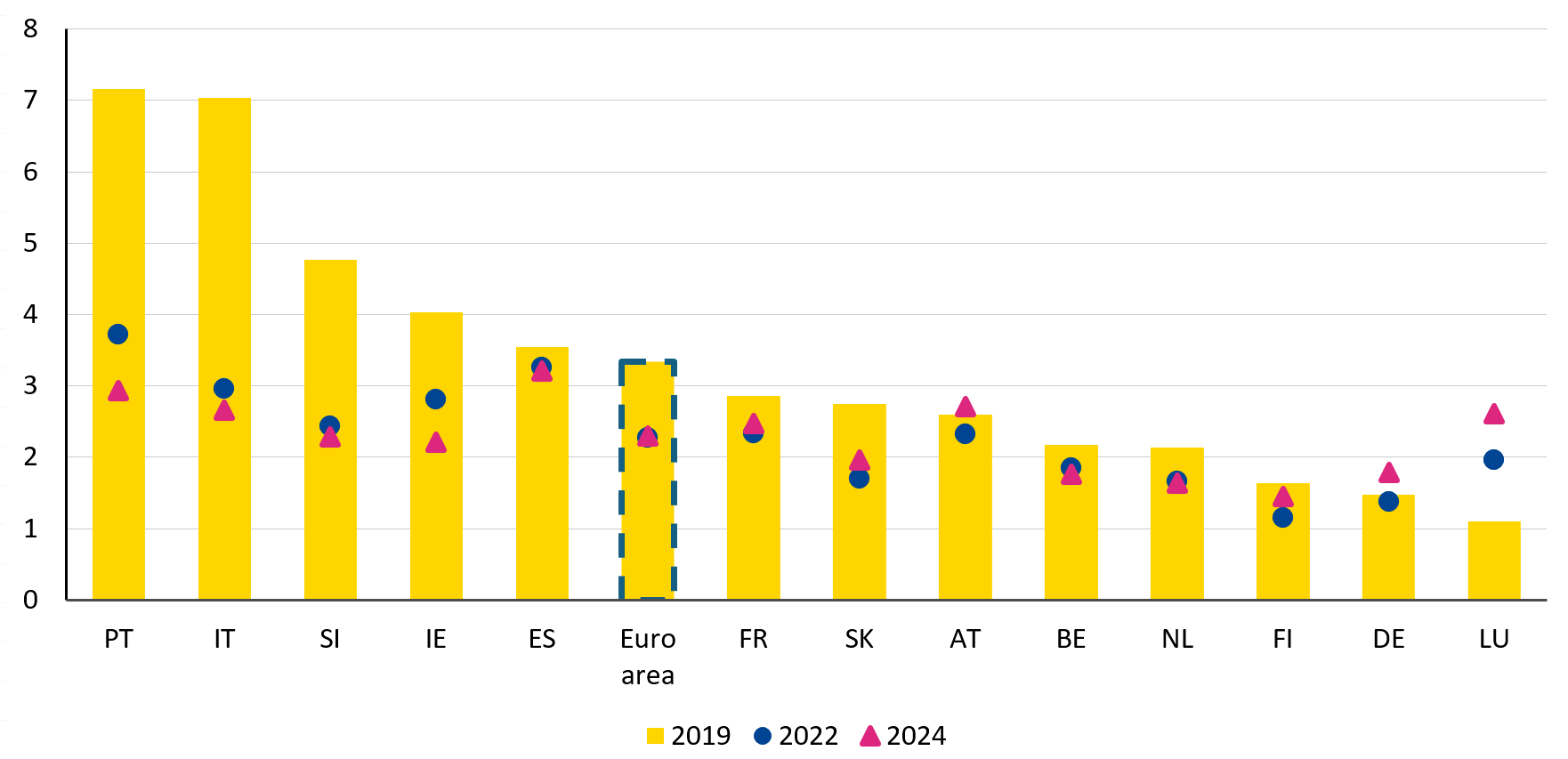

Figure 2, which shows NPL ratios across a selected sample of euro area countries in three different periods, depicts recent increases in NPL ratios even more clearly. Asset quality is currently suffering in those member states reporting NPL levels below the 2019 euro area average, before the pandemic hit. So far, for these countries, the deterioration appears to be concentrated in specific economic sectors, such as commercial real estate. By contrast, countries which historically suffered from high NPL levels, now appear more resilient, showing a continued decreasing trend.

Figure 2: Asset quality is deteriorating in countries with the lowest NPL ratios

(NPL ratios, in %)

Source: ESM calculations based on European Banking Authority Risk Dashboard

Monitoring non-performing loans in a rapidly changing macrofinancial environment

Past crises have taught that it is crucial to closely monitor and assess the evolution of asset quality, particularly now given the prevailing macrofinancial conditions, increasing geoeconomic fragmentation, and sectoral downturns. To ensure crisis preparedness, the ESM has developed an asset-quality-at-risk framework, which allows for forward-looking NPL assessments at the individual bank or system level to help policymakers identify banks at risk of credit quality deterioration in the near future.

This novel framework leverages on the popular growth-at-risk approach. In the setup of the model, we first establish the relationship between NPLs and their macrofinancial drivers and bank-specific characteristics using quantile regressions. Then, the analysis estimates the complete distribution of future NPL ratios conditional on the state of the macrofinancial environment, enabling an assessment of the likelihood of future increase in NPL ratios.

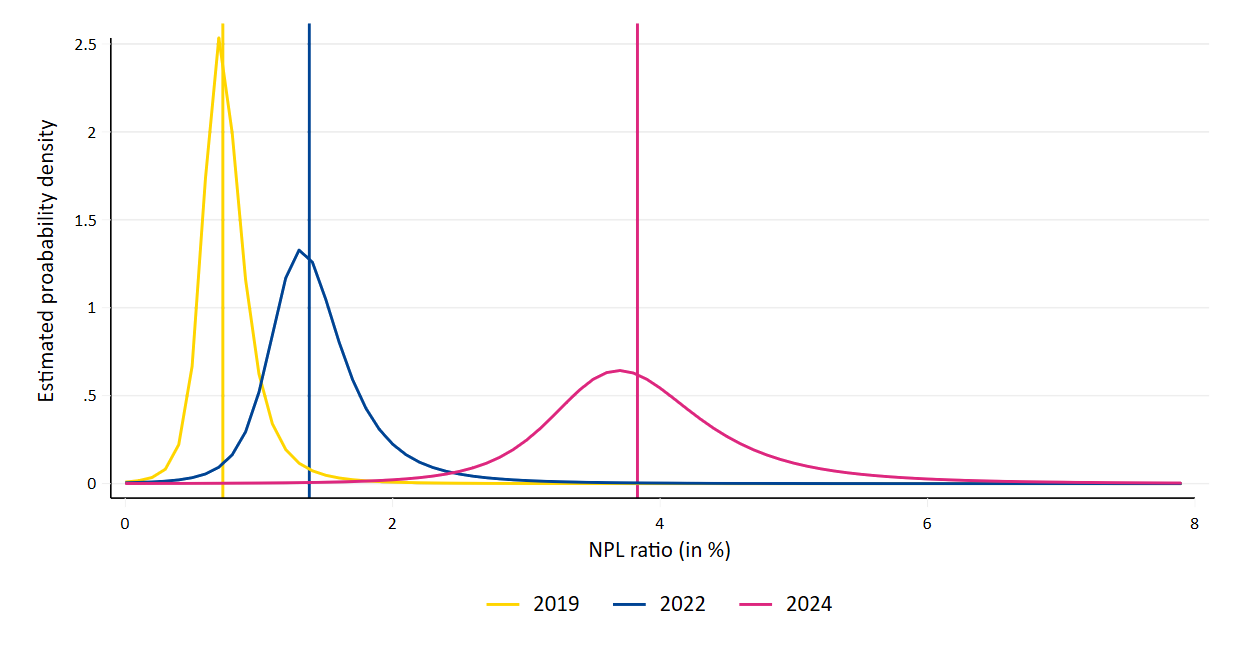

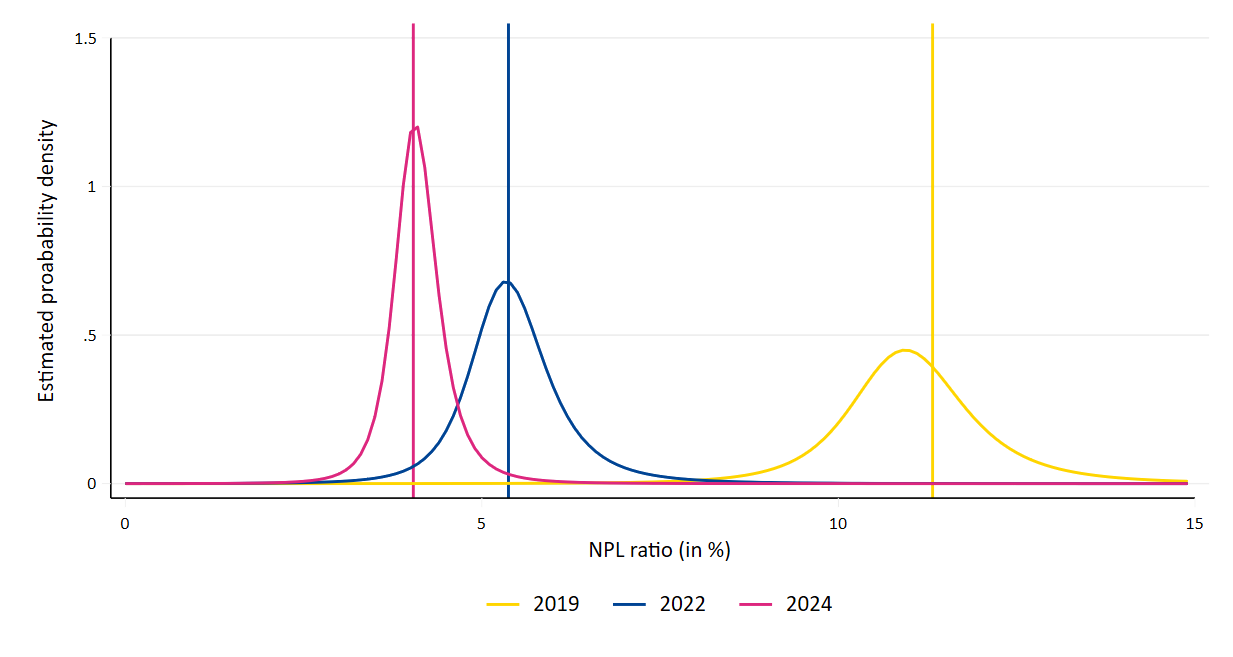

Figures 3 and 4 illustrate the estimated likelihood of future asset quality deterioration for two banks with different exposures to currently vulnerable sectors at three different points in time: before the Covid-19 outbreak, at the end of 2022 when some signs of general deterioration started to materialise across the euro area, and in mid-2024.

Figure 3 depicts the case of a bank with sizable exposure to currently vulnerable sectors of economic activities. Over time, the NPL ratio in the bank increased from 0.7% in the third quarter of 2019 to 3.8% in the second quarter of 2024, as indicated by the vertical line shifting to the right. Further short-term asset quality deterioration is also becoming more likely as the probability density function is moving to the right.[1] Notwithstanding higher NPL ratios becoming more likely, the uncertainty around the estimates is also growing, pointing to the building up of risks for this bank over time, as the potential outcomes become more dispersed.

Figure 3: As NPL ratio rises, future increases become more likely

Note: The vertical lines represent the NPL ratios reported by the bank in the three considered periods, while the bell curves are the estimated probability density functions, indicating the likelihood of different NPL ratios in the next quarter. The bell curve links the possible values that the NPL ratio will assume in the following quarter (x-axis) with the associated likelihood of each possible outcome (y-axis).

Source: ESM calculations

By contrast, Figure 4 depicts a bank that significantly cleaned up its balance sheet over the same period, resulting in an improvement of the quality of its loan book from an NPL ratio of 11.3% in the third quarter of 2019 to 4% in the first half of 2024. These improvements are also associated with a relatively lower likelihood of higher NPL ratios in the short term, as the curve shifts to the left over time. As the uncertainty of the estimates reduces, NPLs become more predictable in the near future, aiding policymakers’ decisions in a more stable system.

Figure 4: As asset quality improves, the likelihood of future deteriorations decreases

Note: The vertical lines represent the NPL ratios reported by the bank in the three considered periods, while the bell curves are the estimated probability density functions, indicating the likelihood of different NPL ratios in the next quarter. The bell curve links the possible values that the NPL ratio will assume in the following quarter (x-axis) with the associated likelihood of each possible outcome (y-axis).

Source: ESM calculations

Despite similar NPL ratios in 2024, we can see how the model predicts different probabilities of future deterioration of the two banks’ loan books, taking into account the different macrofinancial conditions in which they operate and bank specific characteristics such as their business models. This result informs policymakers that enhanced monitoring is warranted for the bank in Figure 3, while the outlook for the bank in Figure 4 is less concerning.

Crisis preparedness requires continuous forward-looking risk assessments

Non-performing loans represent a long-standing policy concern in the euro area. Banks’ NPL ratios are currently well below their historical peaks, which testifies to the effectiveness of regulatory efforts to reduce bad loans. However, some banks with exposures to vulnerable sectors and generally low levels of NPLs are starting to experience some asset quality deterioration.

Although at a system level risks appear manageable, crisis preparedness requires constant forward-looking assessments for potential deterioration of banks’ asset quality. Heightened geoeconomic fragmentation, as well as long-term threats from climate and demographic changes are substantially increasing the complexity and uncertainty of the macrofinancial environment in which banks operate.

This requires all institutions tasked with the mission of protecting financial stability – including the ESM – to be agile and ready to adapt to new emerging challenges. As such, the ESM’s proposed asset-quality-at-risk framework provides a flexible tool to detect in a timely manner possible buildups of vulnerabilities affecting banks’ loan books.

Acknowledgements

The authors would like to thank Paolo Fioretti, Nicoletta Mascher, Rolf Strauch and Cédric Crelo for the valuable discussions and contributions to this blog post, and Raquel Calero for the editorial review.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager