Enhancing Europe's resilience against rising geopolitical risks

Enhancing Europe's resilience against rising geopolitical risks

0:00 minAmidst growing and complex geopolitical challenges facing Europe and the world today, this blog post explores how the European Stability Mechanism (ESM) and the European Banking Authority (EBA) can further contribute to enhancing Europe’s financial sector resilience. It also aims to show how the complementary role of the two institutions can support financial stability in Europe more broadly and contribute to the well-being of European citizens. Geopolitical tensions and geoeconomic fragmentation are shaping the future of the global economy and challenging our conventional understanding of risk. Through continued cooperation and joint analytical work, we aim at understanding the implications of these risks, gauging potential disruptions they may cause, and exploring avenues to mitigate them.

Developing a common understanding around geopolitical risks[1]

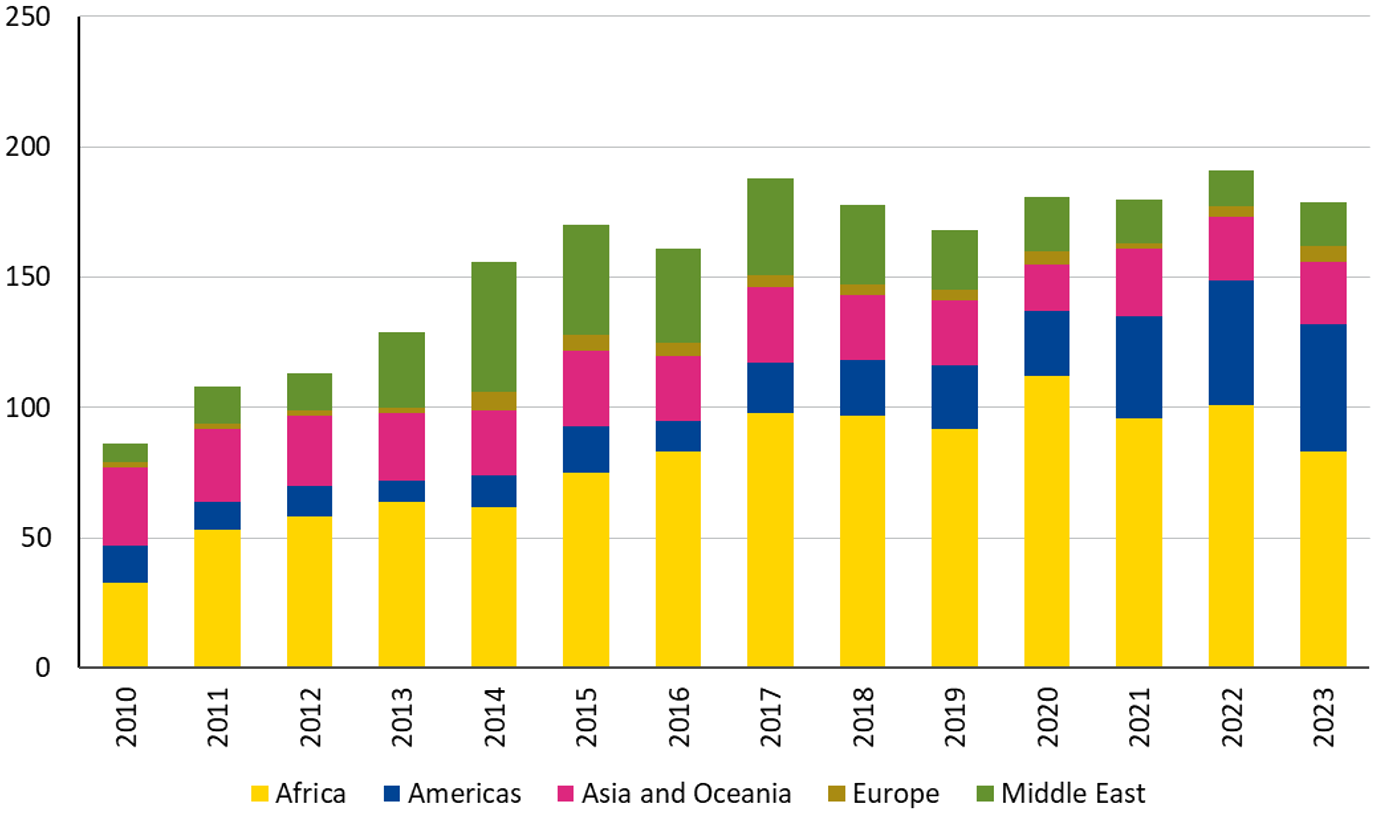

The significance of geopolitical risks has resurged in recent years, notably through the impact of armed conflicts (Figure 1). While conflicts worldwide are a growing source of concern, Europe is now also confronted with a war at its doorstep. Deeper geopolitical fragmentation and economic distress between nations and/or regions, further exacerbate uncertainty and instability.

Figure 1: Number of armed conflicts is on the rise globally

Source: Uppsala Conflict Data Program

Impact of geopolitical risk on the financial sector, with focus on banks

While the financial sector has remained resilient amidst increasing geopolitical risks, individual banks have noticeably been affected.[2] As we advocated in an earlier blog, crisis preparedness is essential, as geopolitical risks are less predictable and harder to quantify due to their interconnected nature.[3]

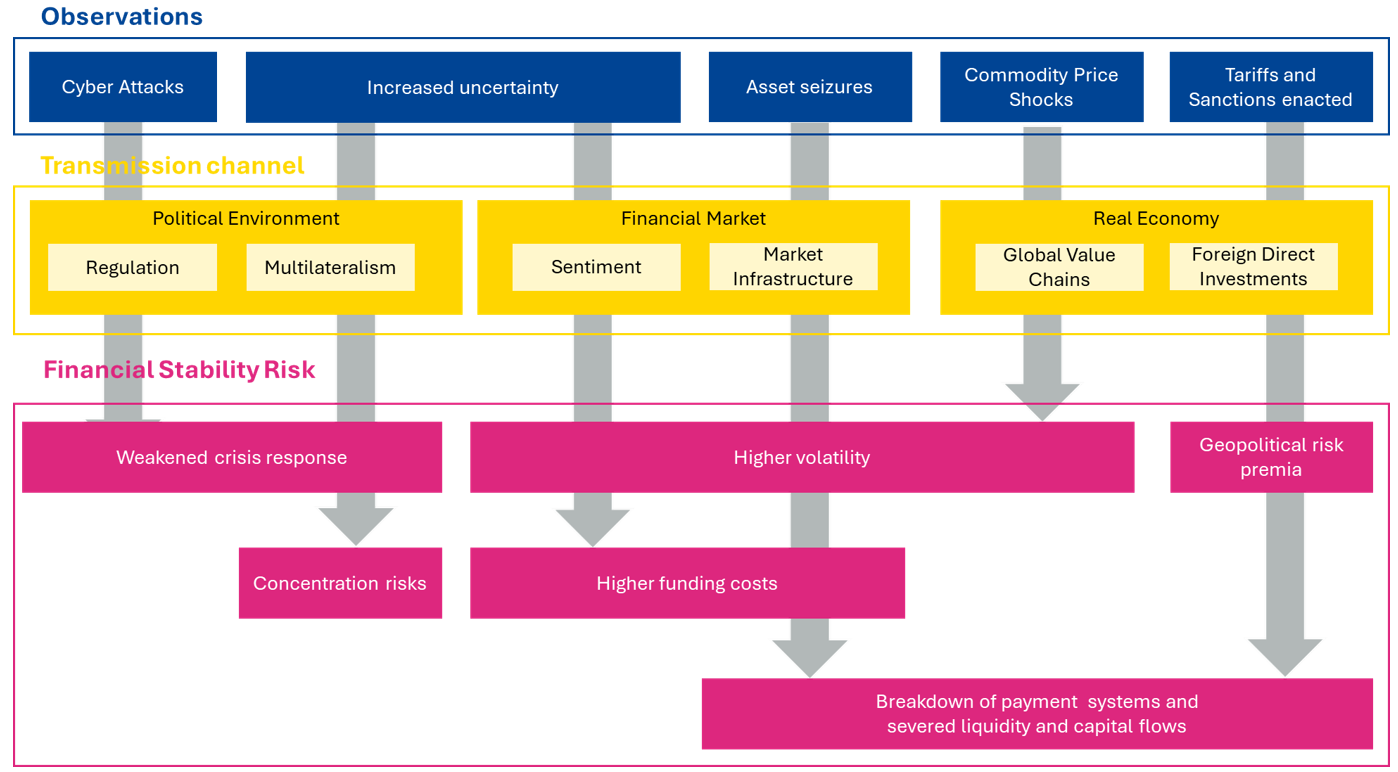

We propose a simplified framework to better understand these interrelated risks and their potential effects on financial stability (Figure 2). To this end, we draw on concrete real-world observations of how geopolitical risk is manifesting itself in the financial sector (blue). We then identify the three transmission channels (yellow) which may propagate and amplify geopolitical risk and geoeconomic fragmentation, thus posing a threat to the stability of the financial sector (magenta). The intensity and scope of the impact depends on the transmission channels.

Figure 2: Observations, transmission channels and financial stability risk from geopolitical tensions

Note: The grey arrows are examples of past observations and of how risk propagated through the identified transmission channels affected financial stability. They are meant illustratively and do not constitute an exhaustive overview of possible ways for geopolitical shocks to translate into financial stability risk.

Source: ESM/EBA

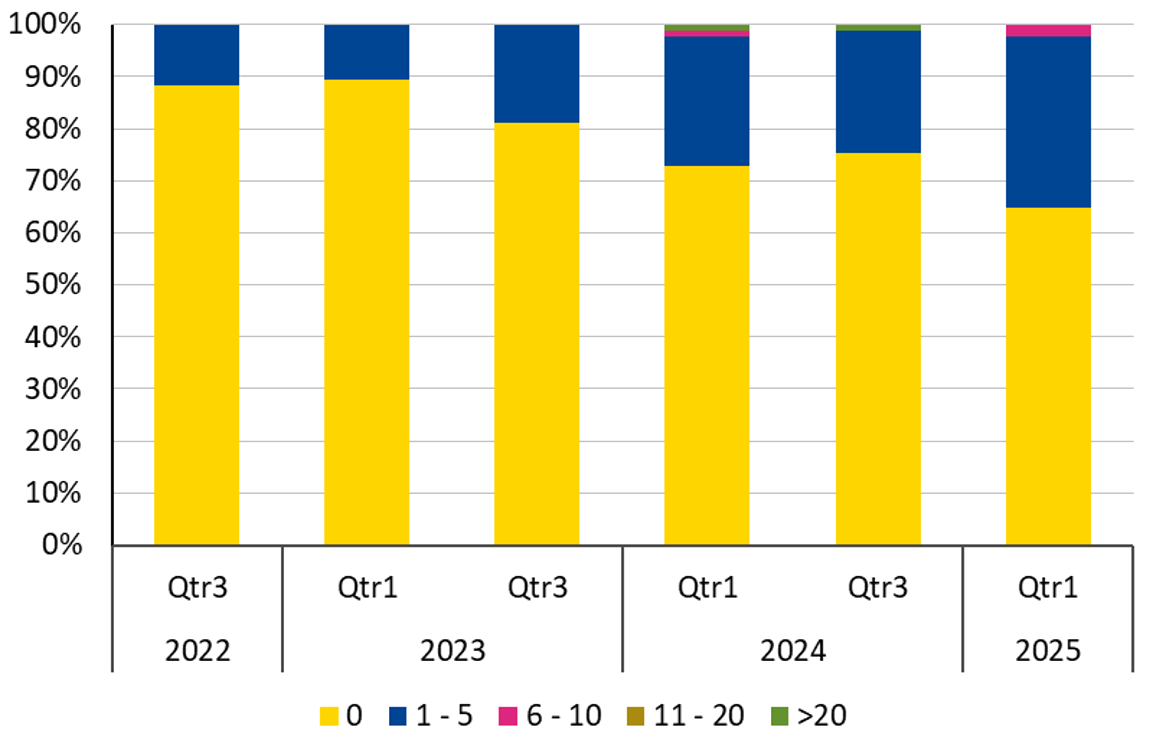

Geopolitical risks affect banks directly and indirectly. Geopolitical shocks and tensions can directly affect banks’ financial position through an increase in credit, market, operational, liquidity and funding risks. For example, geopolitical risk and fragmentation could lead to the deterioration of asset quality. Tariffs, sanctions, or even outright war may affect the quality of assets. Furthermore, the rising number of cyber-attacks can increase banks’ operational and reputational risks and negatively affect profitability. For instance, the results of the EBA’s Risk Assessment Questionnaire show that the share of EU and European Economic Area (EEA) banks that faced successful cyber-attacks has nearly tripled since 2022 (Figure 3). These attacks are deceptive and aim to create chaos and disrupt financial services.

Figure 3: Share of EU/EEA banks reporting successful cyber-attacks

Source: Spring 2025 EBA Risk Assessment Questionnaire

Commodity price shocks as well as tariffs and sanctions directly affect the real economy with a significant impact on financial intermediation. Countries are more interconnected than ever: value chains have become global and foreign direct investment (FDI) has intertwined previously unrelated economies. The advances of this internationalisation are evident. They have created new vulnerabilities: geopolitical events can now amplify commodity market volatility more easily, disrupting complex value chains as shown in an earlier blog. The introduction of tariffs and sanctions creates frictions in the flow of capital and liquidity. This is fuelling a disintermediation of markets, for which investors demand higher returns to cover the added risks.

We also observe indirect effects, in particular via increased uncertainty and the transmission channels of the political environment and financial markets (Figure 2). Divergent political approaches inside and outside Europe increase political fragmentation and undermine multilateral cooperation. Such divergence makes it more challenging to establish common ground and buttress the resilience of the financial system. This is, for example, evidenced by the delay in Basel III implementation in the UK and the absence of a timeline for its implementation in the US.[4] Similar developments are undermining collaboration on climate financing and complicating the commitments of European banks. Increasing fragmentation and deterioration of international cooperation, in turn, can weaken crisis response.

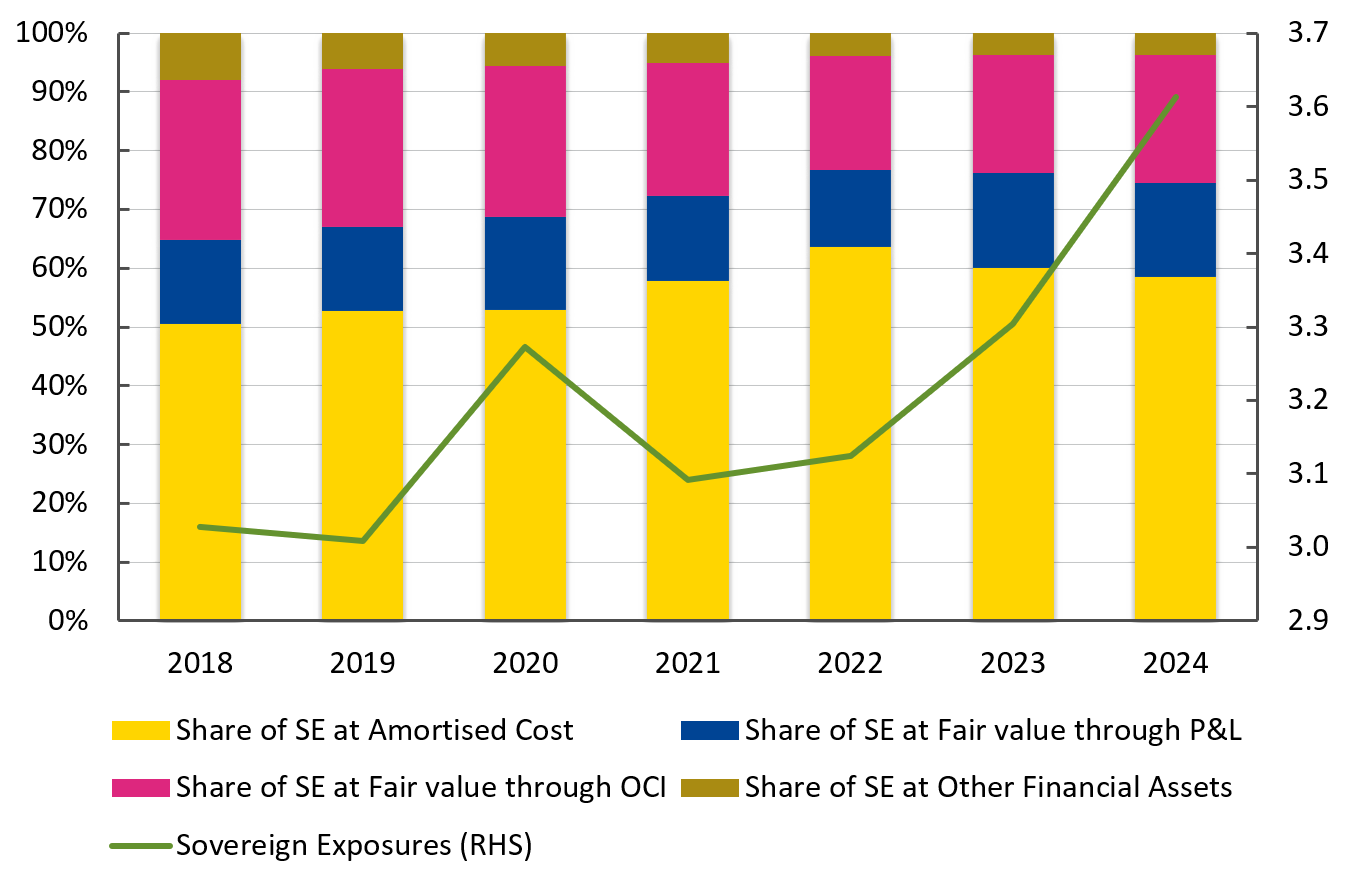

In this environment, increased volatility in financial markets can lead to sudden portfolio adjustments and significant repricing of assets, affecting banks’ profitability. Sovereigns are faced with increased funding needs and higher yields, which, in turn, affect banks’ sovereign holdings. EU/EEA banks are substantial investors in EU/EEA debt. Over €2.7 trillion of sovereign exposures are to EU/EEA countries, with close to 40% of this debt accounted at fair value, implying that losses are recognised immediately (Figure 4). Financial institutions with more exposures to regions in conflict tend to experience elevated funding costs, decreased stock returns, increased stock price volatility, and a rise in credit default swap prices compared to other banks.

Figure 4: EU/EEA banks’ sovereign exposure (SE), over time, composition by accounting valuation and volume in € trillion

Source: EBA supervisory reporting data

Contribution of the EBA and the ESM to addressing geopolitical risks

Besides measures at bank level, the EBA and the ESM can play a crucial role in buttressing system resilience to geopolitical risks. Both institutions reach out and collaborate with other regulatory authorities in the EU and beyond. Doing so ultimately ensures more coordination and hence effective crisis responses.

The ESM with its extensive toolkit can provide financial assistance through several instruments, including precautionary credit lines. Drawing on insights from its market presence, the ESM continues to improve its risk detection capabilities to stay ahead of the curve and identify risks early on. This can allow for timely intervention through precautionary instruments, supporting euro area sovereigns and contributing to financial stability. A lesson of past crises is that early intervention is more efficient than fixing a crisis when it is already in full swing. In addition, the existence of the ESM provides comfort to market participants as it acts as insurance of last resort. This role would be further enhanced by the introduction of the backstop to the Single Resolution Fund (SRF). The benefit reaches beyond Europe, as acting fast limits negative spillover effects on other regions, which in turn minimises backlash and global instability.

As a regulatory, transparency, and risk assessment hub for the EU/EEA banking sector, the EBA can react through regulatory measures in case of a major materialisation of geopolitical risks. [6] For example, the EBA fostered transparency and provided a hub for cooperation when the war in Ukraine broke out. The EBA also provided guidance to banks and supervisors on how they can offer products for Ukrainian refugees in compliance with existing rules.[7] Cyber risk is also high on the agenda, not least reflected in the Digital Operational Resilience Act (DORA). In addition, this year the EBA EU-wide stress test’s adverse scenario assumes a severe escalation of geopolitical tensions, accompanied by a shift towards more protectionist trade policies globally.[8]

Policy implications, recommendations, and conclusions

Geopolitical risks are materialising with increasing frequency, posing significant threats to the financial sector. In the spirit of crisis preparedness, it is imperative to deepen our understanding of these risks. In this blog post, we have outlined these challenges, mapping out the transmission channels and distilling the implications for financial stability.

While banks and firms can mitigate such risks through different measures at entity-level, the EBA and the ESM can play a broader role in protecting the system from the related financial stability threats. Through the complementary monitoring of different risks, blind spots are averted, and interventions can be implemented in a timely manner. The EBA bank stress tests assess the resilience of the largest European banks at a micro-level, while the ESM continuously monitors euro area risks at a macro-level. In addition, to stay prepared for emerging risks, the ESM assessed its financial instruments and is in the process of refining them, ensuring that flexible precautionary instruments can effectively adapt to a wide range of potential shocks. We must remain vigilant in identifying risks and analysing vulnerabilities.

Efforts to mitigate the negative impact of geopolitical risk on financial stability do not stop at merely analysing them. On the contrary, in line with our respective mandates and DNA as multilateral entities, both institutions remain strongly committed to multilateral cooperation to help safeguard global financial stability. This means collaborating with other international supervisory and regulatory agencies and contributing to the work of international organisations such as the Bank for International Settlements, the International Monetary Fund, the Financial Stability Board, and other crisis management institutions in the world. The EBA and the ESM stand ready to facilitate a coordinated crisis response should geopolitical risks materialise and threaten financial stability.

Further reading

Dadoukis, A., Fusi, G. and Sakkas, A. (2025). Geopolitical risk premia in the European banking sector. Working Paper. Available at SSRN

3. Caldara, D. and Iacoviello, M. (2022), “Measuring Geopolitical Risk”, American Economic Review, Vol. 112, No 4, April, pp. 1194-1225.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager