Shock proofing ESM financial stability instruments

Shock proofing ESM financial stability instruments

0:00 minIn a shock-prone world, preparedness and adaptability are key. The European Stability Mechanism (ESM) conducted a comprehensive review of its lending volume, capital adequacy, and financial assistance instruments to assess if these resources remain fit for purpose. The review identified how the toolkit can best be used and further optimised to address the threats to financial stability stemming from the challenges of today, such as climate change and geopolitical tensions.

New types of shocks call for regular reviews of existing tools

Since the sovereign debt crisis of the 2010s, euro area resilience has been repeatedly tested by crises like the Covid-19 pandemic, and the Russian war in Ukraine and ensuing energy price shock. Each blow derailed any economic rebound underway during the recovery phase. Future disruptions could also emerge from geopolitical tensions, cyberthreats, ageing populations, or climate change. The ESM’s role is to preserve euro area financial stability despite these threats, regardless of their origin.

The ESM is the only permanent crisis management fund for the euro area. Its financial assistance instruments have been tested and proven effective during the euro area debt crisis. Given the evolving nature of crises, the ESM needs to ensure that its toolkit and financial firepower remain adequate for a variety of circumstances.

In 2022, the ESM Board of Governors, composed of the euro area finance ministers, requested a comprehensive review of the ESM’s lending volume, capital adequacy, and financial assistance instruments. The ESM staff concluded this review and presented the analytical assessment and findings to the Board of Governors during its Annual Meeting in Luxembourg on 20 June 2024.

How to shock proof the ESM toolkit?

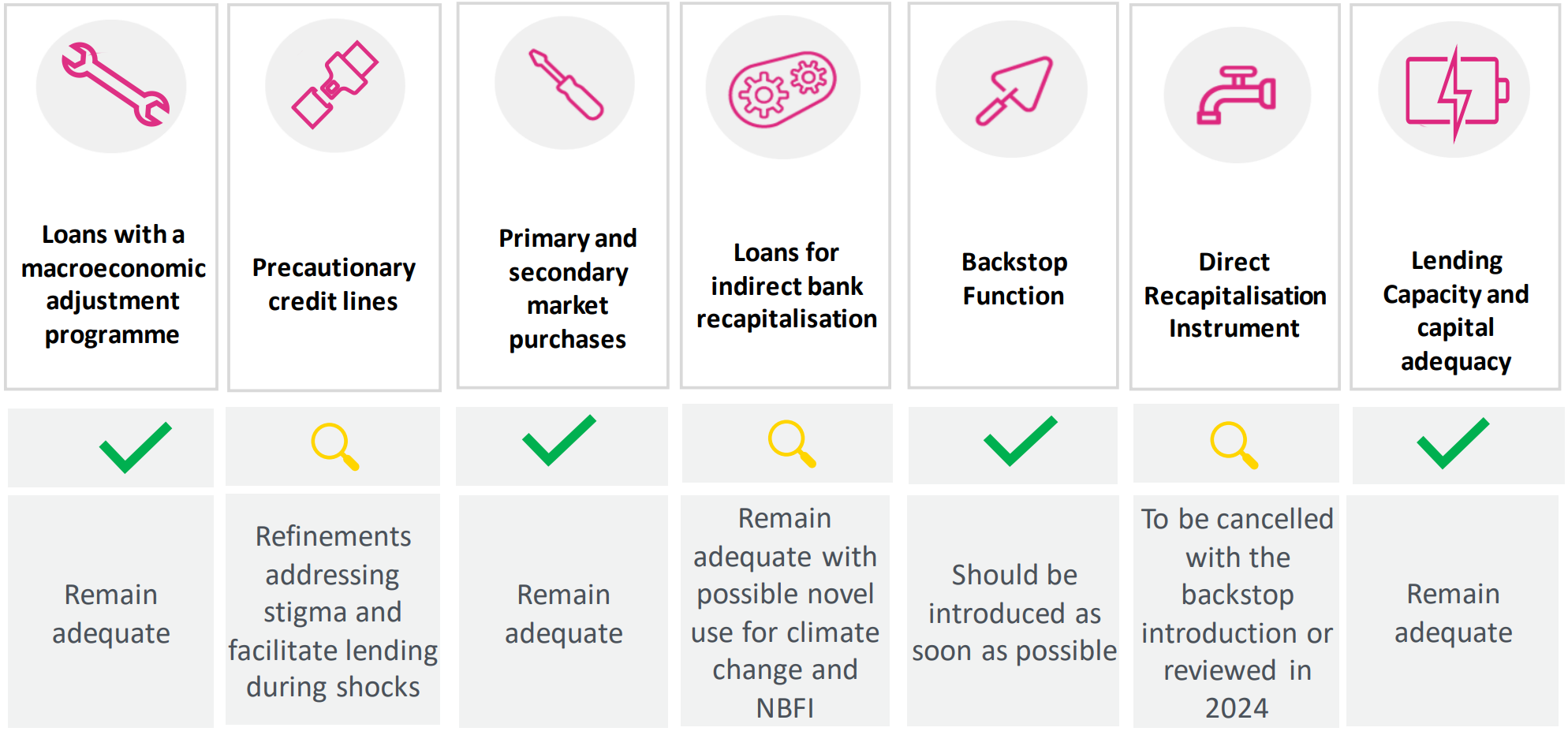

The ESM’s toolkit provides a robust safety net to help withstand economic and financial challenges. The successful outcome of the five macroeconomic adjustment programmes supported by the financial assistance of the ESM and its predecessor – the EFSF – provides evidence for that. Still, given the evolving risk landscape, discussions on how to fine-tune the ESM’s instruments further are timely. Significant changes – such as those that led to the ESM reform and revision of the ESM Treaty, which is pending full ratification – do not seem warranted at this juncture. Using the existing instruments to their full potential, especially if enhanced with the implementation of the provisions set out in the revised treaty, should suffice (see Figure 1).

Figure 1: Summary of findings on the ESM instruments

Source: ESM

The review was an opportunity to revisit the usefulness of the ESM’s precautionary credit lines. Preventing crises is less costly than resolving them, a concept also confirmed by the International Monetary Fund. So, precautionary instruments remain the core tool for crisis prevention because they pre-emptively stabilise economies by signalling economic health and granting access to funding. The ESM precautionary instruments are therefore key to protecting euro area financial stability in a shock-prone regional and global environment. The tools are designed to help countries, whose economic conditions are sound, maintain access to market financing. For example, the ESM’s Pandemic Crisis Support credit line, created in 2020 to tackle the consequences of the Covid-19 pandemic and based on precautionary instruments, helped calm markets despite not being used, partially fulfilling its purpose.

Nevertheless, the ESM drew lessons from the lack of request for this tool, which was due to political stigma and the availability of other instruments provided by European institutions that supported sovereign market access during that period.

Additionally, the European Union’s (EU) new economic governance framework entered into force in April 2024. This important reform has an impact on the way the ESM grants financial assistance as access to these credit lines is tied to criteria linked to the EU fiscal rules.

As part of their findings in the toolkit review, ESM staff has proposed some adjustments to the precautionary loans.

First, the eligibility criteria for precautionary instruments should be aligned with the new fiscal rules once the revised ESM Treaty has entered into force. This will ensure that any ESM Member requesting support and complying with the agreed EU fiscal framework and other eligibility criteria, can qualify for the highest tier instrument: the Precautionary Conditioned Credit Line.

Second, to address the hesitation by some countries to apply first, increase the efficacy of its instruments and ensure they are better suited for future shocks, the ESM could introduce group requests of financial assistance.

Third, a new instrument could be developed – within the existing or revised treaty – to provide support for new external shocks. This would validate the sound economic policies of the affected Members and eliminate the risk that drawing on the credit line would be perceived as a sign of weakness.

In addition to precautionary instruments, existing instruments, like the Indirect Bank Recapitalisation Instrument, could also be used to address new risks. Although created and used before the introduction of important banking union elements, this tool remains relevant to address systemic issues affecting several financial institutions at the same time, possibly across multiple countries. It could also address financial stability risks stemming from climate change and from non-bank financial institutions.

The revised ESM Treaty also includes the common backstop for the Single Resolution Fund, which can be introduced as soon as the treaty enters into force. It is an important pillar of banking union. The Single Resolution Fund, which is financed by banks, will have to repay the ESM loans. This way, a bank can be resolved without causing financial instability and without costs to taxpayers, making the introduction of the backstop even more urgent.

The powerful shield of ESM’s lending capacity

Staff also reviewed the ESM’s available lending capacity, which currently stands at €422 billion out of the €500 billion maximum amount. It is set to fall by €68 billion after the introduction of the backstop for the Single Resolution Fund.

The ESM’s maximum firepower is supported by its subscribed capital of €708.46 billion, of which €80.97 billion was paid in by the euro area member states with the remainder committed as callable capital.

The maximum lending capacity has been kept unchanged since inception of the ESM. Hence, a gradual decline of the ESM’s financial firepower can be expected over the long-term relative to the euro area gross financing needs. Still, the improved overall safety net, regulatory provisions, and ongoing efforts to pursue further advances through capital markets union and banking union provide additional buffers and may reduce the need to activate ESM’s stability support. Therefore, the ESM’s maximum lending volume and authorised capital stock remain adequate at present.

ESM stands ready

Europe’s deeper integration has happened during times of crisis. The ESM, born as a response to the sovereign debt crisis, is a living testament to this. In addition, the EU and its Member States have ramped up spending on common initiatives and instruments to shield and help recover from various shocks.

At a time when euro area resilience faces the threat of new challenges and public debt levels remain high and divergent across countries, inspecting EU-level financing is unavoidable. With this review, the ESM is doing its part to contribute to the euro area’s ability to weather future shocks, remaining agile and looking at ways to adapt to Members’ evolving needs.

Acknowledgements

The authors would like to thank Dušan Kovačević for his support with this blog post, and Raquel Calero for the editorial review.

Further reading

International Monetary Fund (2023), Review of the Flexible Credit Line, the Short-Term Liquidity Line, and the Precautionary and Liquidity Line

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Authors

Blog manager