Population ageing and productivity: The innovation channel

ESM Briefs is a concise presentation of research by ESM staff members, helping readers better understand and navigate current economic policy debates. More about ESM Briefs

Abstract

Demographic changes in the euro area have led to a decrease in the working-age population in the recent decade, and long-term projections point to the labour force shrinking further in the future. Population ageing can have a significant impact on the real economy in the short and long run.

As the workforce gets older, the economy’s capacity to innovate diminishes, leading to a permanent loss in labour productivity. In addition, the insufficient adjustment of real wages to this decline of labour productivity can further intensify the deterioration in competitiveness and long-term growth.

Policies redirecting euro area investments towards projects that enhance potential growth through innovation and human capital can counteract these effects. The commitment of Member States to achieve the green and digital transitions and implement the necessary reforms, combined with the availability of the EU funds (NGEU), presents a crucial opportunity for euro area countries to address the consequences of ageing and other mega-trends challenging Europe’s future.

Acknowledgements: The authors would like to thank Rolf Strauch for his valuable comments and contributions, and Karol Siskind for his editorial support.

Demographics, productivity, and the innovation channel

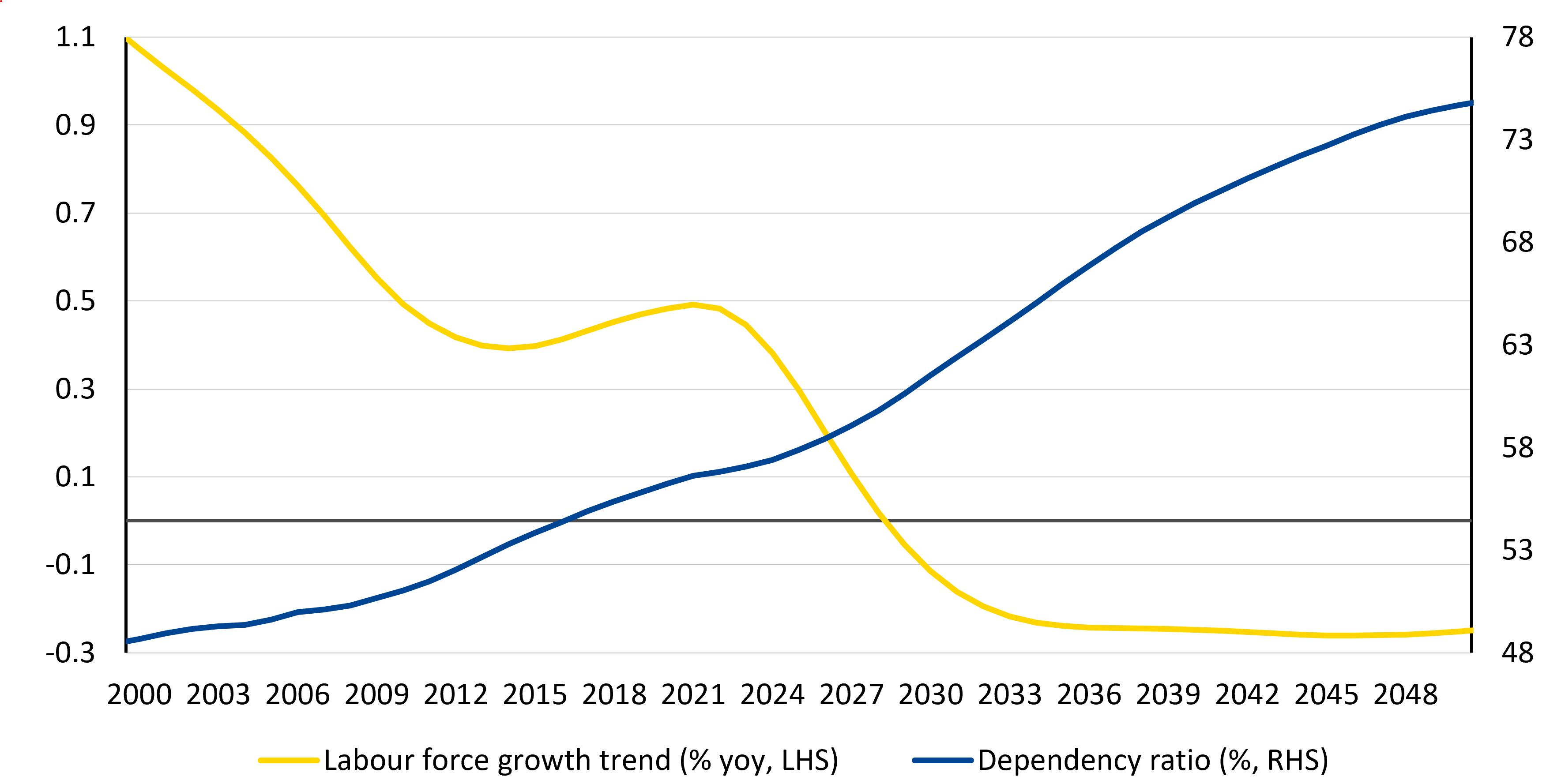

The ageing of the euro area (EA) population has led to a significant and protracted structural change in the labour force. Due to ageing, the growth rate of labour supply in the euro area has been consistently declining since the 2000s (Figure 1). According to available forecasts,[1] this trend is expected to continue in the upcoming decades. Conversely, the dependency ratio,[2] the share of the economically dependent population per working-age population, has shown a historical upward trend that is projected to continue in the coming decades.

Figure 1: Labour supply growth trend (%) and dependency ratio (%); historical data & long-term projections

Source: ESM calculations based on EC

As the population continues to age, it is crucial to understand the broader economic impact. A better understanding of the economic implications of this structural change can help policymakers to evaluate the magnitude of the challenge we are facing and design adequate measures to address it. This study uses a semi-structural (SVAR) model to identify the effects of a permanent change in the dependency ratio for a set of selected relevant economic variables.

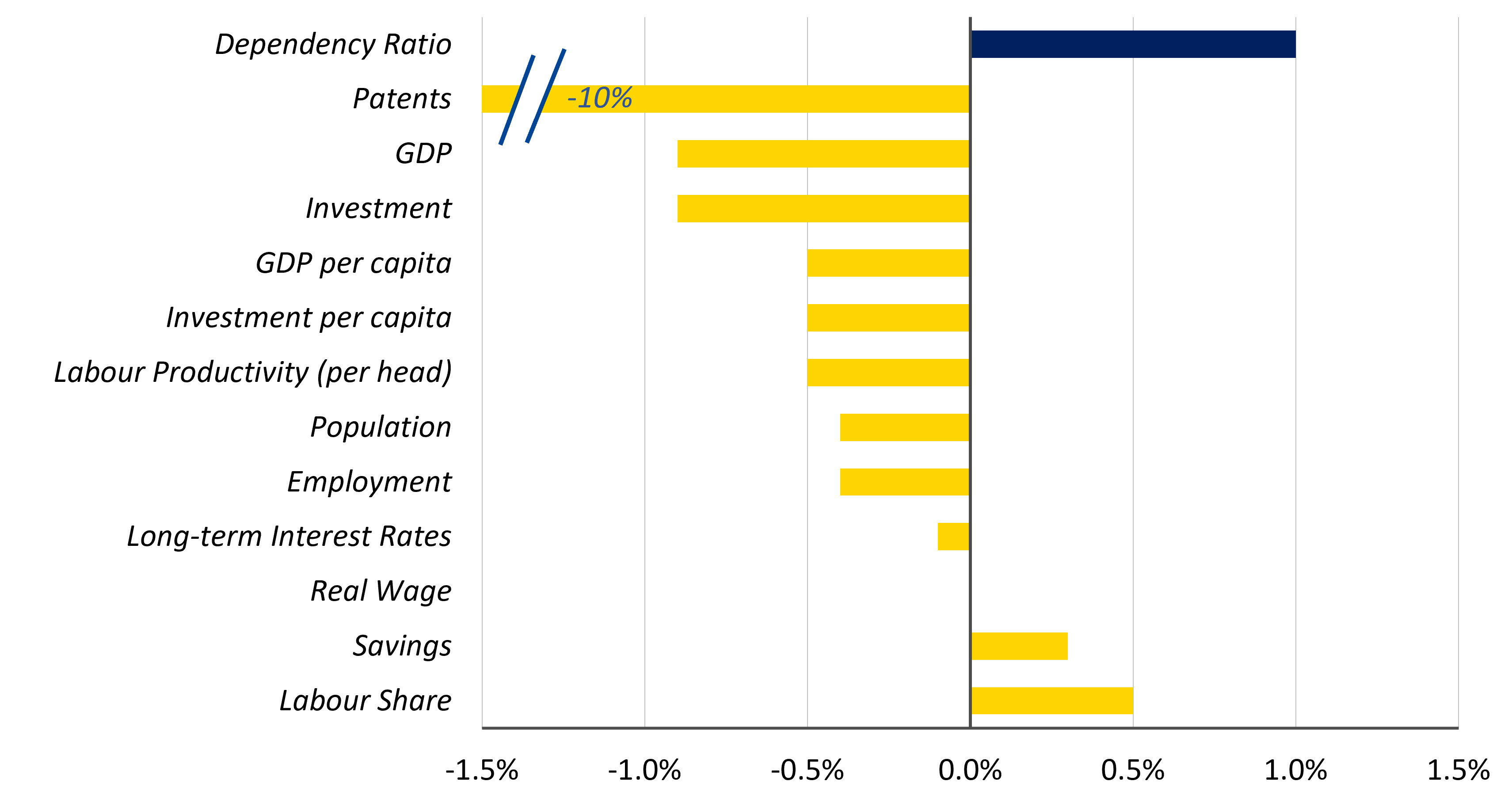

According to our estimates, the adverse population dynamics are expected to lower euro area productivity permanently. Table 1 presents the long-term estimates of an unfavourable demographic shock that results in a one percentage point increase in the dependency ratio in the long run.[3] As one would expect, the population reduction directly leads to a decline in GDP over time due to lower employment growth. However, the decrease in output surpasses the decline in employment by a significant margin, reducing investment and per capita GDP. Maestas et al. (2023) obtained similar estimates for the US using a different methodology.

Table 1: Long-term impact of an adverse demographic shock

Notes: The shock is normalised to increase the dependency ratio by 1pp in the long run. For all variables (except the real wage and investment per capita) considered here, zero is not included in the 16-84% posterior probability mass. Source: ESM Calculations

An inverse relation between ageing and innovation hinders technological growth and overall productivity.[4] According to the simulations, the increase in the dependency ratio is associated with a significant and lasting reduction in patent applications, which proxies technological innovation. Furthermore, the persistent decrease in GDP per capita and labour productivity indicates a negative feedback loop from ageing to technological growth ("endogenous growth" dynamics). As the population gets older and the proportion of retirees increases, the innovation capacity of the economy is reduced, which hinders technological progress and labour productivity (Aksoy et al., 2019).

In addition, the rigidity of real wages to adjust to the downside intensifies the negative impact of ageing on productivity. Although real wages decrease as a response to the demographic shock and the initial fall in productivity, this reduction is statistically insignificant in both short and long-term contexts. This lack of substantial adjustment in labour compensation hampers the economy’s ability to offset the initial decline in labour productivity. Consequently, the (real) labour share, i.e., the labour costs per unit of output, experiences a notable increase, aligning with economists' perspectives that an ageing workforce may generate inflationary pressures.

The enduring rise in real marginal costs implies a deterioration in the region's external competitiveness, with adverse implications for the current account.

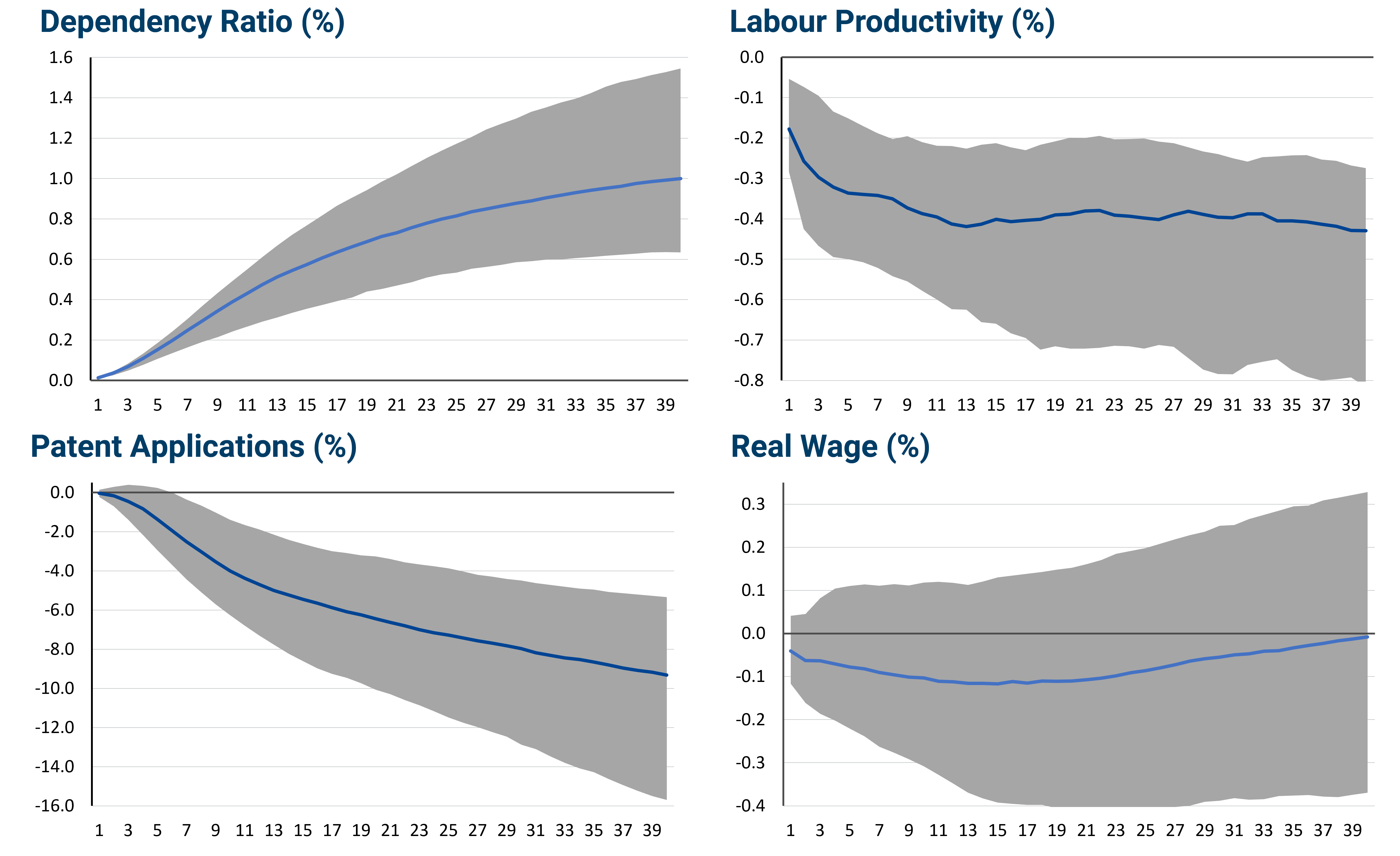

The transition towards the new equilibrium will not occur instantaneously, taking almost a decade to materialise due to various economic frictions (Table 1 and Figure 2). This implies that the complete picture of adverse demographic dynamics discussed in this note may still elude us.[5]

Figure 2: Effect of an adverse demographic shock: transition paths to the new equilibrium

Notes: The shock has been normalised to increase the dependency ratio by 1pps in year 10. X-axis denotes quarters. The blue solid line and shadow illustrate the pointwise median and the 16th-84th percentiles of the posterior response distribution to an adverse demographic shock. Source: ESM calculations

Future productivity may also be influenced by other developments and emerging trends, with migration dynamics and artificial intelligence as potential mitigating forces of the ageing effect. Our analysis abstracts from the potential benefits arising from migration and the deployment of artificial intelligence (AI) technologies. As populations age and labour forces decline in certain countries/regions, strategic migration could help to reduce workforce imbalances. Additionally, AI technologies can enhance productivity and fill gaps left by demographic changes, particularly in sectors with labour shortages. By combining the strategic movement of human capital with the transformative power of AI, societies can adapt more effectively to demographic shifts and foster resilience in the face of changing population dynamics. [6] Therefore, the estimates discussed in this previous section can be viewed as an upper bound.

Addressing the productivity gap: Comparing investments and reforms in the US and euro area

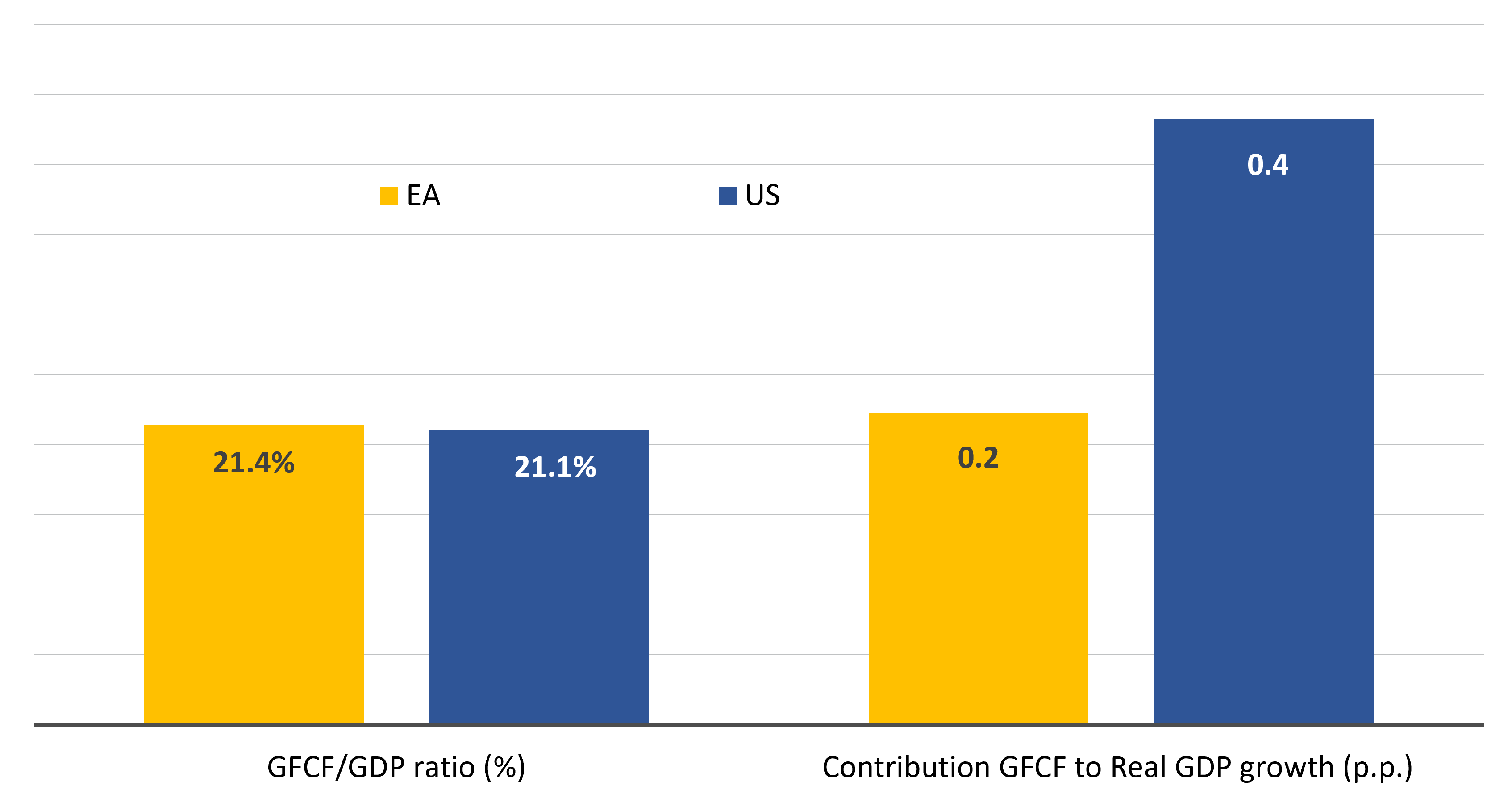

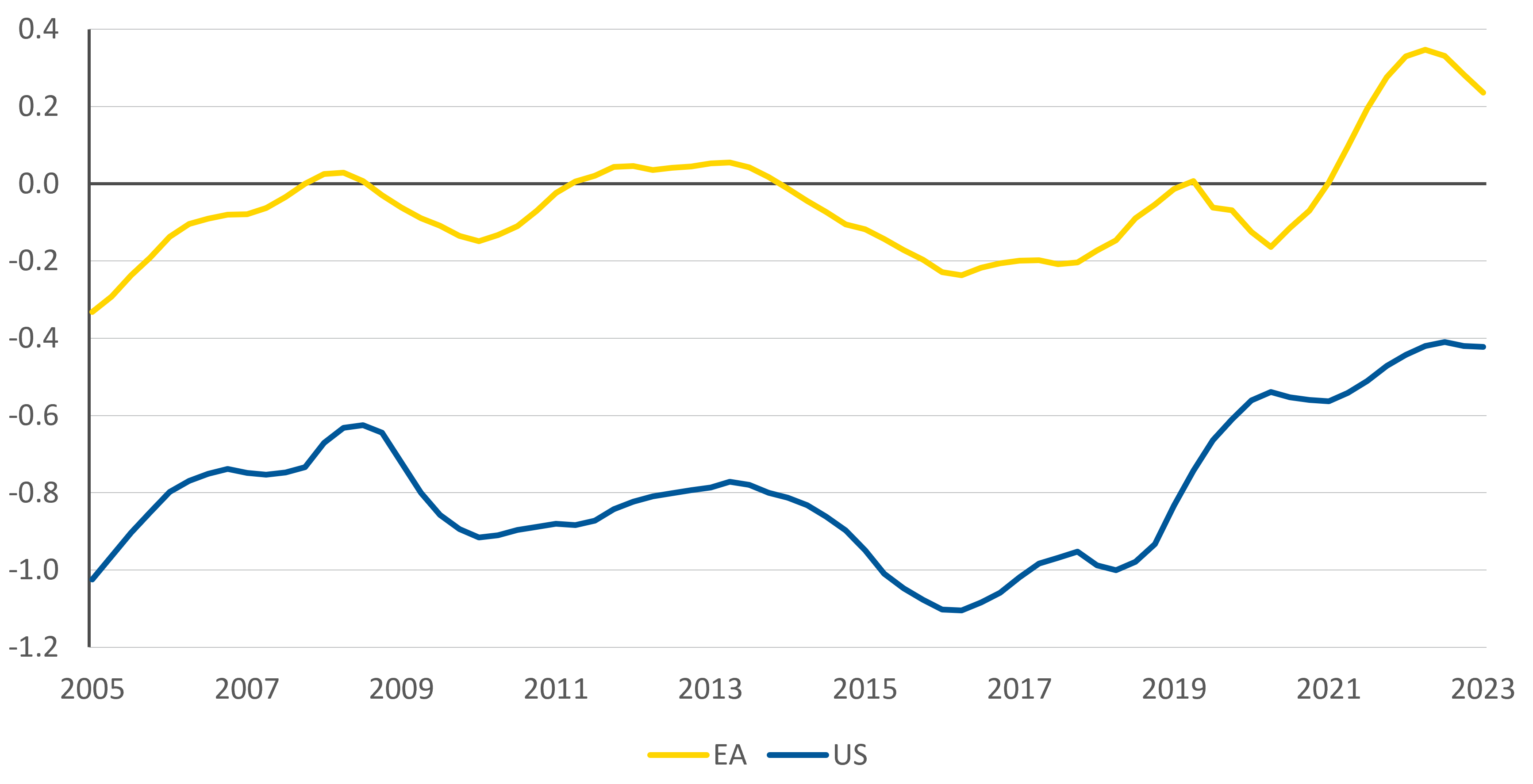

Increasing investments in “growth-enhancing” projects could contribute to counteracting the decline of labour productivity due to ageing. A comparison between the euro area and US investment performance in the last decades proves insightful in this respect. As depicted in Figure 3, since the early 2000s, both economies dedicated, on average, a similar percentage of GDP to investment. However, in terms of contribution to GDP growth, US investments seem to have been more productive. The evolution of the relative price of investment (an indicator of the productivity of capital[7]) on both sides of the Atlantic leads to the same conclusion: the US investment projects, on aggregate, outperformed their EA counterparts. These visuals clearly highlight the heterogeneity of investment projects, underscoring the point that not all investments yield equal results. It also shows the upside potential for the euro area of reallocating investment resources towards a more “growth-enhancing” profile.

Figure 3: Gross fixed capital formation: % of GDP and contribution to annual real GDP growth (EA vs US, average 2000-23)

Source: AMECO

Figure 4: Relative price of investment, long-term Growth (%)

Source: Haver and ESM Calculations

Growth-enhancing investment are those projects that expand potential supply.[8] All investments contribute to the enhancement of an economy's productive capabilities. In instances where such improvement does not occur, an investment expansion merely signifies a redistribution of spending and resources from consumption to investment (i.e., housing investment), with no consequential increase in potential supply. Clearly, these types of projects do not offer the means to alleviate the adverse effects of demographic shifts on societies. Consequently, investment policies must focus on identifying large-scale projects capable of expanding the economic aggregate's potential supply while encouraging private sector involvement in these endeavours.

These growth-inducing projects are intricately linked to research and development (R&D) initiatives and the expansion of human capital. Investments in R&D and human capital lead to innovation and technological progress, generating a virtuous circle between investment and potential growth. A similar positive effect on potential growth could occur through adequate structural reforms, in particular, those that aim to improve the investment environment and the removal of frictions.[9]

The European Commission’s Green Deal Industrial Plan offers some good suggestions for these reforms, including simplification of the regulatory framework for the “net-zero” industry, as well as speeding up investments and financing for clean-tech production in Europe. This would happen both through public financing and further progress on the European capital markets union to unlock private funds.

Moreover, labour market initiatives aimed at enhancing skills, both green and digital, would help with the potential labour shortages faced by some strategic industries. One proposal in this regard is the creation of Net-Zero Industry Academies, mentioned in the Green Deal Industrial Plan.

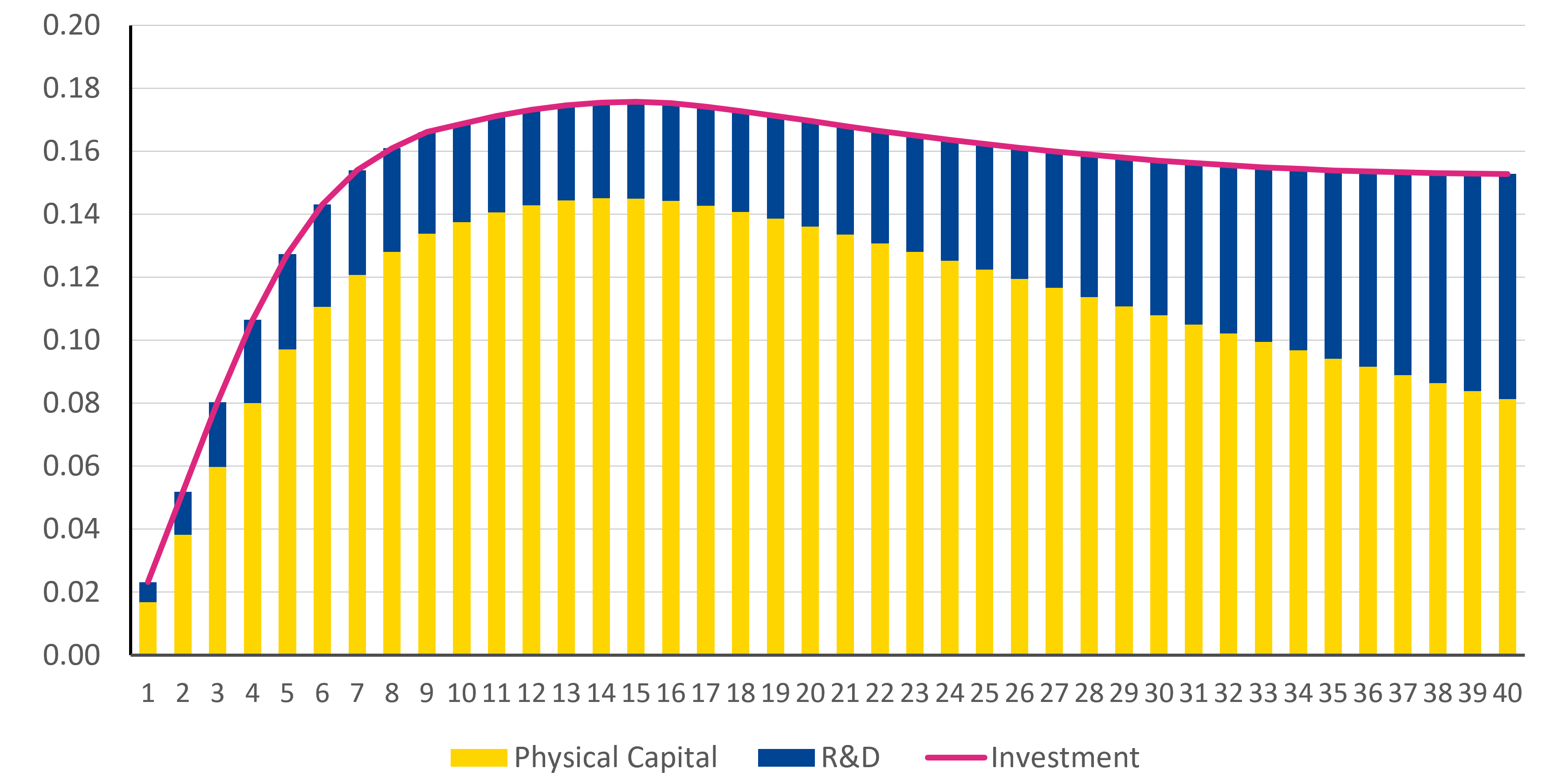

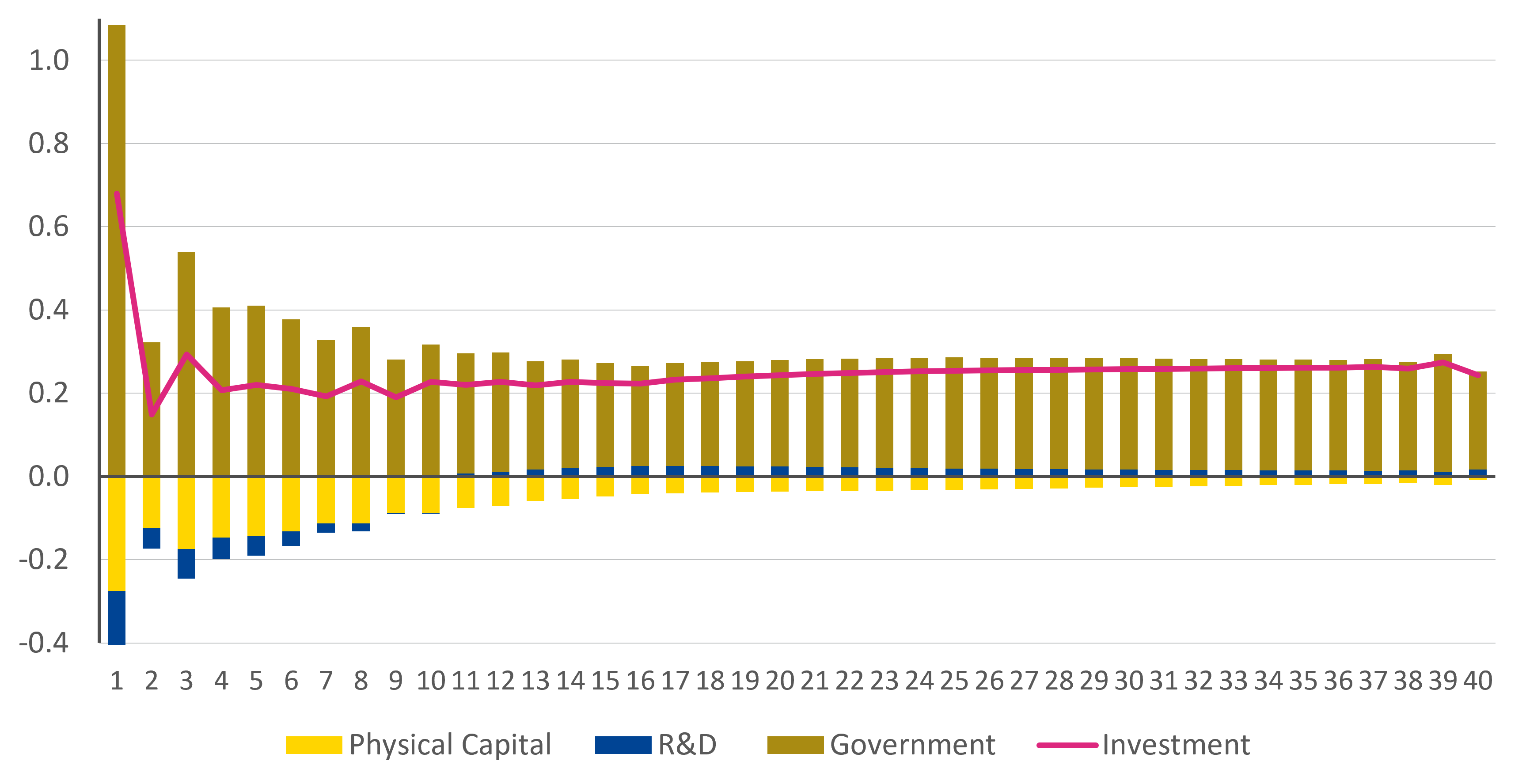

A permanent increase of investment in “growth-enhancing projects” of around 0.2% GDP would offset the fall in labour productivity induced by a 1 pp rise in the dependency ratio. [10] In the case of private (tangible and intangible) capital investment, it will need to rise by 0.16% of GDP (Figure 5) to restore the productivity loss caused by the 1 pp permanent increase of the dependency ratio. Government investment (alone), on the other hand, would need to rise marginally more (0.2% of GDP) to achieve the same results, as public investment “crowds out” private investment marginally (Figure 6). The fiscal cost of public authorities undertaking growth-enhancing investment policies to counteract the productivity lost by population dynamics is small and short-lived.

Figure 5: Private investment (% GDP) needed to offset the fall in labour productivity induced by 1pp permanent increase in the dependency ratio

Notes: The simulations are based on DSGE with endogenous (learning by doing and R&D) growth mechanisms calibrated for the EA. The x-axis denotes quarters. Source: Haver Analytics and ESM calculations

Figure 6: Public investment (% GDP) needed to offset the fall in labour productivity induced by 1pp permanent increase in the dependency ratio

Notes: The simulations are based on DSGE with endogenous (learning by doing and R&D) growth mechanisms calibrated for the EA. The x-axis denotes quarters. Source: Haver Analytics and ESM calculations

Conclusion: A call for policy action - innovation, human capital and structural reforms

In light of demographic challenges, it is essential to enhance long-term productivity in the euro area through strategic investments and necessary reforms. Initiatives already in progress, such as the European Commission’s Green Deal Industrial Plan, or, more broadly the national Recovery and Resilience Plans (RRPs), have the potential to foster long-term growth through innovative investments. The success of these efforts, however, hinges on the efficient execution of these plans.

Initiatives like NGEU and the Green Deal Industrial Plan could mark a turning point for the euro area in adopting more ambitious measures to improve its growth prospects. [11] The transition to sustainable practices holds the potential to drive economic growth and job creation. Investments in renewable energy and eco-friendly technologies can spur innovation, enhancing overall productivity. This shift also diversifies EA industry and opens new markets, fostering a more resilient economy. Aligning economic strategies with sustainability goals can create a virtuous cycle where growth and environmental well-being reinforce each other.

Beyond the public funds committed, private sector involvement is crucial to achieve a successful green transition, an efficient allocation of resources, and a more productive economy. Further deepening of the single market, with the development of capital markets union and the completion of banking union, would be a key step in this direction. Along with the implementation of the new fiscal framework, both are vital ingredients in creating a stable environment for promoting high-quality private investment.

Further reading

"Demographics and financial stability", Presentation by Rolf Strauch, ESM Chief Economist

[1] 2024 Ageing Report. Underlying Assumptions and Projection Methodologies, European Commission, 2023.

[2] The dependency ratio refers to the share of population aged 0-14 years and 65 years or over, to population between 15-64 years (also referred to as working-age population).

[3] K. Bodnár and C. Nerlich (2022) express very similar concerns about the impact of ageing labour on productivity, wages, and labour share. Our analysis complements and adds statistical support to their arguments.

[4] Related studies are Aksoy et al. (2019), Kara et al. (2024), Kotchy and Bloom (2023) and Maestas et al. (2023).

[5] The responses of all nine variables (dependency ratio, population, real wages, GDP, employment, investment, long-term (10y) government yield, private savings (% of disposable income) and patent applications), as well as their posterior distribution, are reported in the technical annex. The empirical model also includes additional variables not discussed in the text, such as savings and the EA long-term interest rate. These variables are left “constrained”, and their responses can be used to assess the plausibility of the identified shock.

[6] The details of how of AI and human capital strategies could lead to higher potential growth in the EA can be found in the EC’s report EU competitiveness: Looking ahead, known as “the Draghi report”.

[7] Investment deflator divided by GDP deflator. Related studies (among others) are Fisher (2006), Justiniano et al (2010) and Grortz et al (2022).

[8] Again “the Draghi report” (its in-depth analysis) is a good reference point for understanding the type of investments that can enhance potential growth.

[9] Pfeiffer et al. (2023) use a structural model similar to the one considered in this note to estimate the potential benefits of the EU reforms undertaken as part of the post-pandemic recovery plans. The authors reveal significant benefits even if Member States only narrow the gap with the EU’s best-performing countries by half. However, our note’s focus differs, as our exercise aims to illustrate the gains from modernising EA production.

[10] We do not explicitly discuss the types of investment but developing environmentally friendly technologies similar (or even superior) to carbon-intensive ones could be an excellent example. Green technologies that do not increase production costs will also limit the use of inefficient taxation aiming to reduce (inefficient) emissions.

[11] The overall envelope for the EU’s green industrial transition could reach around €680 billion (5% of 2022 GDP) in the current decade, subject to the speed and scope of the uptake of available loans and grants.

Authors

Manager ESM Briefs